To invent next-generation cyber insurance—as a widely available, widely cheap, mass-market product—insurers must first resolve long-standing structural complications. We have identified three levers to achieve this:

Mitigate Risks to specific individuals through enhanced cyber security

Right size Exposure, especially during cyber disasters

Enlarge Earn access to capital for cyber underwriters

We covered the known ones – risk mitigation through improved cybersecurity – previously. Today we are shifting from individual risk to risk portfolios and exploring two very different levers: risk adjustment and technical capital growth.

At the moment, cyber can cause very colossal losses, both from exceeded limits and from catastrophic events affecting many policyholders at the same time. But if they can limit losses and tweak the overall capability — adjust the risk so you might be able to talk about it — insurers can dampen that dynamic. This, in turn, can encourage access to the capital that the line needs and permanently reduce market costs.

Recover costs through decisive incident response

Critical early scrambling as cyber disasters develop – just like natural disasters – can help stem colossal single losses. So how do insurers waive this?

First of all, funds can be directed to containment through efficient disbursement. Some innovators such as Parametrix and Qomplx even take the parametric model into cyberspace and bypass the full provisioning assertions/adjustment direction to present ‘bridge’ liquidity neatly in front of the primitive processes being performed.

Additionally, insurers (and brokers) need to blend dedicated incident response services and products into their offering – so buyers have access to an expert suggestion once an incident is detected.

Since Many buyers already pay for incident response independently of insurance, however there is another model that insurers may be able to keep in mind, perhaps as an alternative to pipe insurance into a bond convert. As mentioned, cybersecurity and cyber insurance can potentially be inexpensively integrated into a managed safety layer – and managed detection and response (MDR) or security operations center as a provider (SOCaaS) would be natural extensions to this and invent additional synergies.

In the 2022, the global SOCaaS market is ~$19m, but will map $m from 720, driven by demand for specia lized cyberforensics, regulatory compliance and crisis communications services and products.

Great cyber exposure through Spruce skill assignments

Any initiative to limit cyber claims is welcome. On the other hand, colossal single losses aren’t the explicit robust dynamic at play within the line.

We used to refer to cyber as “unnatural exertion” – qualified to cause the same devastation in an insurer’s e-book as a hurricane or earthquake, but supposedly a lot less easy to diversify.

A valuable touchstone is encountered in most current discussions about pandemic insurability. With Covid- 349 governments have shown their vitality in shutting down entire sectors and markets in a single day – no doubt triggering business interruption (BI) claims from every policyholder in the e-book. If Covid- represents the borderline case of diversification, where is cyber in terms of comparability? Some fast skills, no doubt.

Certainly, while cyber risk hasn’t been able to fragment NatCat’s seasonal rhythms, that doesn’t mean there aren’t rhythms that wearers can adjust to ensure stability in their portfolios .

First of all, cybercrime is a de facto financial system in its own right, with hackers opportunistically switching between more than one avenue of attack – which no longer necessarily corresponds to all cyber classes. A few years ago, the most popular cyberattack was fact-breaking, but breaches have since declined in the face of a major ransomware bubble. Now, in an added twist, let’s consider “double extortion” cases that combine ransoms with leaks. and making that valuable for insurance is yet another bridge. On the other hand, this may even help insurers to disrupt the internet in its perils – quite unlike the following like floods, earthquakes and wildfires in NatCat. Each brings an entirely different loss profile, with implications for pricing, diversification, exclusions, and floors.

Actuary vs much like the ransomware arena

Ransomware is often mentioned in the context of exclusions and floors. As for incompatibility in the case of data breaches: the loss here is proportional to the breach size (e.g. the type of buyers affected), the ability to secure borders can essentially be based on the largest breach size. Cyber ransoms meanwhile could potentially be arbitrarily large. So, safe limits for insurance policies and data breaches are exhausted by ransomware – when ransomware is added to the protection without additional understanding.

That’s clear. You can even think about adjusting insurance for ransomware – with higher premiums and more capital. On the other hand, coverage is already expensive and capital is already limited. With such limitations on the likelihood that the industry can rob, a modest reduction in ransomware exposure will no doubt come with an increased ability toward expanding wildly different protection styles and customer bases as the industry seeks actual returns.

An additional arena is the hackers’ scope for smarter pricing, as “hacktuaries” see the sweet space for atmospheric ransoms. Especially as ransomware coverage becomes more authorized, lifelike ransom demands can potentially move toward limits, requiring higher premiums and larger limits—a vicious cycle that best serves to fund hackers.

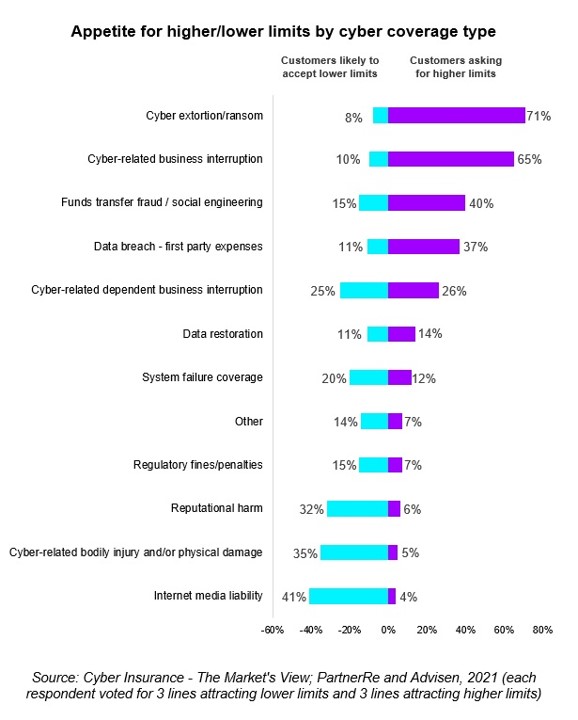

In response, some insurers have come a long way in cutting ransomware funds. On the other hand, any attempt to fully exclude ransomware is likely to meet policyholder resistance: according to the latest understanding of cyber underwriters and brokers, “cyber extortion/ransom” coverage has the greatest appetite for larger limits and the least appetite for limit reduction .

Removing cyber aggregations through AI-driven portfolio valuation

Finally, there are no quick fixes to cyber’s diversification arena. Even for people who might also play with the stability of the cyber classes you support, the risks within each class remain highly correlated.

For all cases, successful ransomware attacks are always vulnerable to hitting a high percentage of policyholders due to the ease with which hackers can copy and paste an identical attack template. On the other hand, the reproducibility of attacks might decrease over time as organizations’ operational and security environments evolve more and more individualized – what capability that risks within an identical class, like ransomware, will eventually decompose.

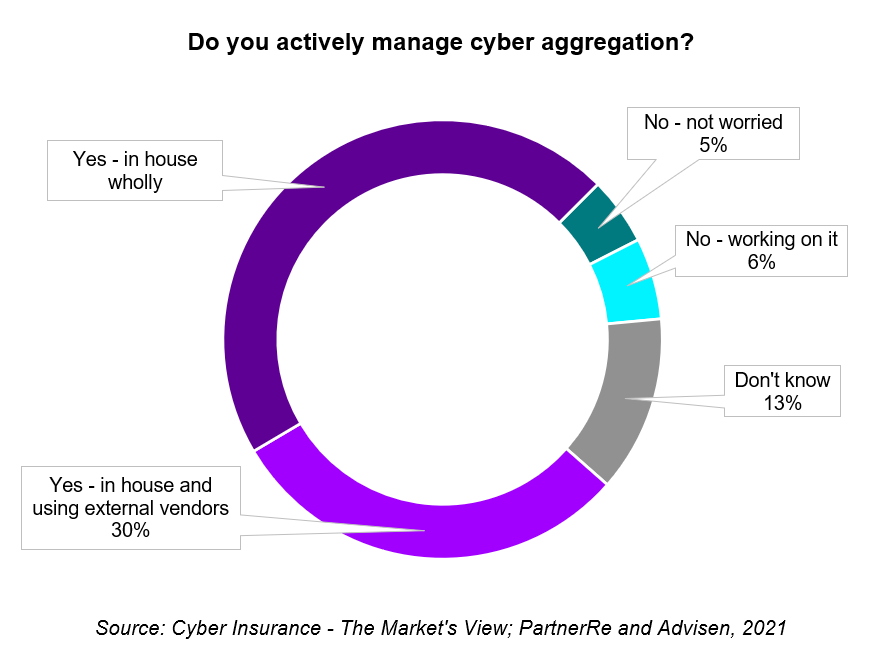

This is speculative, so it will take a gigantic portfolio assessment – likely AI-driven – to unequivocally determine where aggregations are occurring and what factors are actually valuable to achieve better diversification. Currently, three quarters of cyber underwriters are actively compiling cyber aggregations:

Over time, portfolio valuation will become more accepted and mature – as will its closer integration with risk options and pricing. This means insurers can optimize benefit allocation, improving capital costs and thereby reducing costs for nearby businesses.

We started this sequence by observing this cyber insurance as we mark it is damaged – with high costs choking the scale and improvements within the line. The portfolio-stage interventions outlined here – segregation of individual cyber risks plus data-driven approaches to diversification – will do powerfully to “break the line”, especially when combined with enhanced cybersecurity to mitigate individual risks. That brings us to the final piece of the puzzle: subscribed capital.

As you make it up, subscribed capital becomes

reach. At the heart of the no longer easy cyber market, there is a lack of capital for writing cyber risk – it represents a final limit for the market increase. So how is this solved?

The contaminated data states that there is no quick fix for rising skills: as long as cyber risk is viewed as a speculative investment, underwriters will seek it as opposed to its capital to grow disadvantageously. As with any prospect, the area needs to aim to be truly investment grade; At best, then, investors will circulate cyber into the bread-and-butter portion of their portfolios, with the higher and more usual allocations that entail.

The coolest data is that cyber no longer will remain a speculative investment indefinitely.

The entire lot we mentioned in this sequence – finest cybersecurity, fast incident response, Begre catastrophic risk mitigation, aggregation management – takes us closer to a product that potentially delivers actual returns at scale. Like a puzzle, the leisure and the last fragment slots solve themselves; Fixed cyber underwriting and capital will pour in due.

Capital will come from many directions. Poison cyber (re)insurers who have “cracked” the line will write more industry. Similarly, carriers currently lending the wings – those with tiny appetites for hypotheses, we shall inform – will feel better prepared to invent their debut.

With the undeniably gargantuan amount of cyber risks waiting to be written, another asset is likely at play in the assembly of future requirements. Transactions in insurance-linked securities (ILS) at this level must have been rare on the internet, largely reflecting the speculative nature of the probability. On the other hand, tons of topics advise on long-term cyber risks for outdoor investors:

With interest rates low, cyber brings returns – decoupled from broader money markets and no doubt cat assets too

While primitive cat risks can trap investor capital for many years if claims arise, cyber is more short-term – allowing investors to circulate in and out relatively easily

Not anymore today simple market returns will continue to spur financial invention. Let’s even take a look at Cyber Cat Bonds in the years to come – assuming the market can find acceptable solutions to value them. Sidecar-like constructions are now being tried out by a handful of well-known carriers.

In the short term, carriers must use a pragmatic option for scaling the line. It is no longer just a question of milking the conditions that are no longer easy today; Nor is it about going broke and fixing the entire world’s cyber complications. By pulling the levers mentioned here, insurers can reinvent a viable cyber market from scratch: increase the number of buyers with some degree of cyber security, expand sub-lines, and ultimately arrive at a range of mass-market products.

We hope you enjoyed this sequence – for more information, discover our cyber insurance. To continue discussing any of the suggestions we’ve covered, please earn eagerly.

Essentially, rescue the most up-to-date insurance industry insights, data and comparisons directly to your inbox.

Disclaimer: This train material is for common Data applications ready and destined to be little more pretty than a session with our professional consultants. 45033

Post a Comment

0

Comments

Post Top Ad

Archive

Author Details

My Name Celestine Philip, A USA base blogger, certified Digital Marketer, Online Coach on Blogging Tips. Google Publisher since 2017. Thanks for visiting my blog

Click/tap to view the next picture.

Click/tap to view the next picture.

0 Comments