In our final paper, we examined one of the most prominent structural considerations affecting today’s cyber insurance market, including terrible cybersecurity hygiene, aggregation probability and capital shortages. Before cyber insurance can actually develop into a mainstay of the digital financial system – as a widely available, largely cheap and price-stable product – these considerations must be made. We have diagnosed three key levers available to insurers:

Mitigate individual threats through enhanced cyber security

Rightsize engagement, particularly in the event of cyber disasters

Extended access to capital for cyber underwriters

Pulling these levers now will not unlock billions in cyber bounty overnight. Nevertheless, this may temporarily result in a functioning cyber market that will almost certainly be scaled sustainably – without the outrageous volatility that the line is currently experiencing at most. We’ll see each of these levers in our upcoming posts, starting today with the first: Systems to mitigate threats through enhanced cybersecurity.

Insurers need to incentivize a brand new baseline in cyber likelihood reduction

It is a standard law of insurance that harmful probability brings with it higher premiums – and this is where the one-component manufacture cyber insurance for a ramification of corporations, particularly micro and medium sized enterprises (SMEs) is , unaffordable. However, lower the probability and lower rewards will be ready. Fortunately, in the case of cyber attacks, there is a factual basis that is fairly easy for companies to collect.

Many cyber attackers use low-tech or no-tech approaches – such as social engineering – to gain unauthorized access to buildings, records, data and programs. Well-communicated cybersecurity assurances and employee training will be credited to this fact sweeping the best hacking opportunities off the table.

These “soft” mitigations involve the dilemma that the impacts are thoughtful to quantify and replicate conservation costs. Regardless, it’s almost a win for insurers – or brokers – to make cybersecurity educational materials and resources freely available to policyholders through a portal or something similar.

Hackers can, of course, transfer through the gears and raise larger tech tools for more durable targets. But even here, a reasonable amount of cyber defenses can cover a merciful distance. There is a wide variety of cybersecurity software tools – from firewalls and antiviruses to encryption and password managers – to enhance basic security, all available on a mass-market basis.

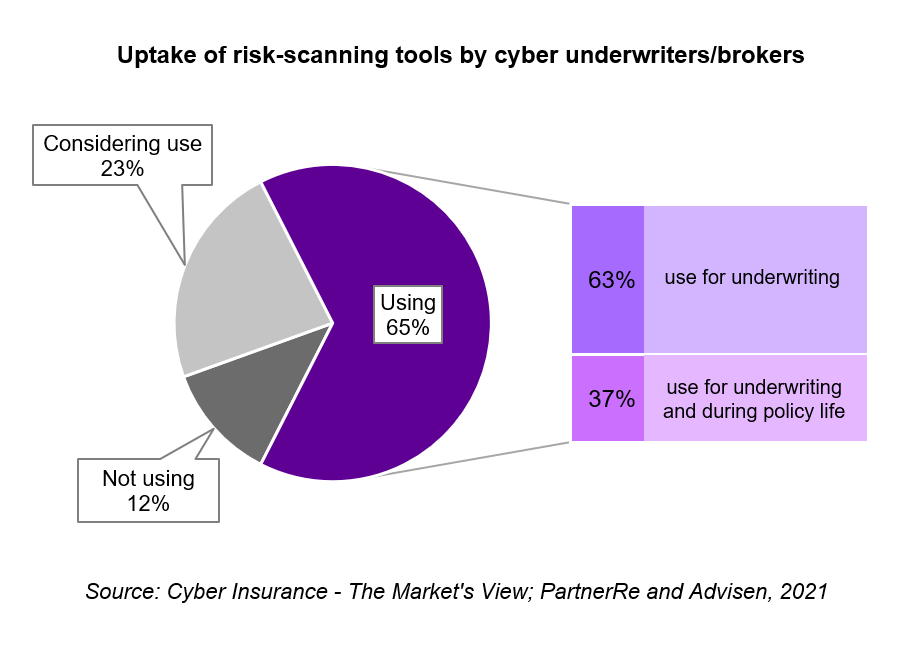

Within the case of comparable “hard” damage reductions, the damage effects can be quantified without further ado. Packages are both energetic and non-energetic, and so they imply broadly the same from one implementation to another. Because of this truth, important loss comparisons can be made between different insurance groups, which opens the door to more sophisticated pricing probability scanning tools (both in celebration of the first anniversary and via distributors) for underwriters to give themselves some degree of time reading of the to give defense of companies:

Click/tap to explore larger list. Offer: Cyber Insurance Coverage – The Market’s Gaze; PartnerRe and Advisen, 995

This type of diagnostic tools will assist insurers on the purchase of security software; in the meantime, the risk of damage is also excluded. All of this promotes likelihood reduction among policyholders, leading to greater cybersecurity hygiene, reduced losses and, as a result, lower premiums for the market as a whole – a chart that goes against solving the line’s affordability situation.

Against Timely Cyber-Likelihood Engineering with Digital Twins

Introducing a brand new baseline for factual cybersecurity an obvious gain, but it’s certainly not the end game – because hackers enjoy extra gears dumb. According to the story that they will tap into a global community of illicit capabilities and repeatedly probe corporate perimeters over many months, static defenses—even when most practical—do not permanently increase the likelihood.

As we saw in our chart above, cyber likelihood scanning is now well established. Nonetheless, of these players, risk scanning at the time of underwriting is the most productive % Do this too, all diagrams in which through the following protection life cycle. Repeated or continuous monitoring helps ensure that specific cyber defense systems are updated and these new vulnerabilities are addressed as quickly as possible. As such, we are looking for records of data from this application to show wider adoption in the years to come.

Within the kill, diagnostic scans will give way to predictive analytics using digital twins.

Digital twins are the appearance of a reproductive community, the chart also varies “what if” possibilities tested while the exact community remains untouched. This enables continuous stress testing to uncover weaknesses in capabilities before they arise. And by combining digital twins with self-learning AI, security teams can simulate the beginning-end nature of a cyberattack, with a preppy program producing untold inaccurate surprises when it’s reproduced – but not exactly now! – Community.

Successful right here is a skill to stop before the hackers by becoming a hacker yourself, taking care of the downside of your agreement with weaknesses first and any exploitation prevent from them. Concretely, the nature of clean scenario planning with digital twins yields a roll of hazards assessed through accidents and business impact, empowering security teams to successfully assign sources – and in theory, at least, insurers to dynamically determine probability.

Up to now, insurers have been boring when it comes to introducing digital twins and mostly sat in the experimental phase. Nonetheless, cybersecurity is proving to be a serious driver for the adoption of digital twins more broadly – so perhaps the cyber sector is just a factual discipline for insurers to outline their efforts. Either chart, 37% of Insurance managers seek records of their organizations’ massive investments in digital twins to improve over the next three years (Accenture Insurance Protection Technology Vision ).

Combination of cyber insurance and mitigation through ecosystem partnerships

Organizing a worthwhile pricing model for a chosen piece of security software—and then offering that worthwhile ticket with all the charts in the footprint of the software—switches previously priced ones inquiries and gives cyber insurers a quick position advantage in a largely unaffordable market. The quickest chart to represent these price objects is customer scaling and gigantic exposure to different types of security software. And ecosystems offer a promising course forward.

In recent years we have seen ourselves as cyber insurers in accomplice with cyber tech corporations to provide risk management and risk transfer in a single bundle.

The effectiveness of bundling also opens up opportunities for other actors in the distribution chain. Perhaps, with their customer proximity and industry specialization, Managing Frequent Agencies (MGAs) and brokers are just better positioned than carriers to protect the likelihood management functions and all considerations surrounding the exchange of highly accurate customer data.

Duvet may also just be made even closer to customers in the form of embedded insurance – with cyber-tech companies promoting white-label duvet through their software suites. And with global spending on cybersecurity companies and products as a total cyberinsurance GWP dwarfed, it can only be more natural for retailers to get their duvets through cybersecurity firms than their cybersecurity through duvet firms.

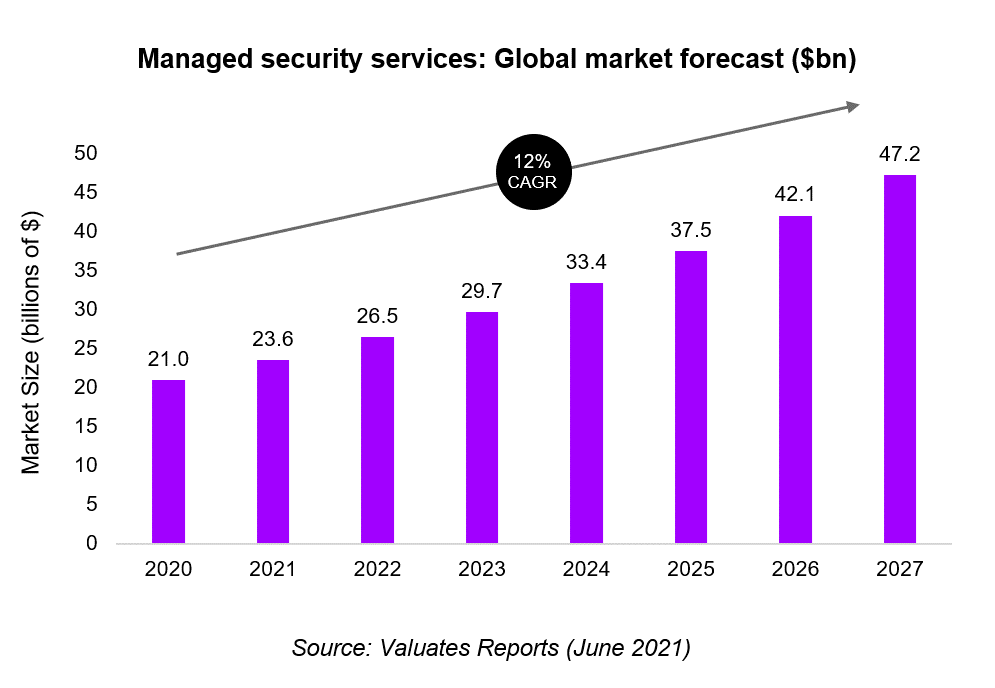

The final winners of this trend may not be individual tech companies, but rather moderately managed security companies (MSSPs). These may also represent an efficient diagram to bundle more than one discrete cyber company and products and distribute them to small and medium-sized enterprises (SMEs).

Click/tap to select a larger list to discover .

Offer: Value Experiences (June )

Managed security evolved because of the history of SMBs not leveraging the sources for an integrated cybersecurity feature. They’re also not well served by one-to-many relationships with hundreds of different tech distributors, brokers, and insurers. By comparison, a one-to-one relationship with an MSSP may also enhance SMBs’ current cybersecurity software combined with probability-adjusted insurance costs in a capability that’s both contractually simple and low-friction.

Cyber insurance protection is now at an inflection point and ready for some quick muttering. Additionally, check out our latest document, Cyber Insurance Coverage: A Compelling Course to Mumble.

LEARN MORE

Through increased mitigation – whether through actuarial monetary incentives or the distribution of security companies and products – cyber insurers can reduce the likelihood of losses on individual accounts. This would do well to drive down the value of duvets and grow the cyber insurance market through wider adoption. And mitigation is precisely one lever to improve today’s model.

In our next post, we think of two additional levers insurers can pull: risk adjustment and expanding access to underwriting capital. Wi r believe that by taking action across more than one spectrum, insurers can lead to a cascade of safe changes in the cyber market – in favor of the broader digital financial system. To learn more in the meantime, save our solid cyber insurance document. And if you have any extra tips to discuss about this series, please get in touch.

Weave the latest insurance business insights, records, data and learning straight to your inbox.

Disclaimer: This annotation material is equipped for common dataset data functions and is simply not meant to be dated moderately than a session with our experienced consultants. 44547

Post a Comment

0

Comments

Post Top Ad

Archive

Author Details

My Name Celestine Philip, A USA base blogger, certified Digital Marketer, Online Coach on Blogging Tips. Google Publisher since 2017. Thanks for visiting my blog

{kind=link}

0 Comments